UK Outlook – Lags could push Bank of England to faster cuts

Key points

- Although BoE policy appears to have peaked, rising mortgage rates will continue to tighten monetary conditions throughout 2024

- We see the economy on the cusp of recession in 2024, with risks skewed lower. Growth should accelerate somewhat in 2025

- Given the policy lags, we see the BoE easing from August next year – and more quickly than expected

Lags threaten recession

The UK has had a difficult year but the past 12 months have seen inflation fall to 4.7% from 11.1%, the economy avoid recession and gilts outperform their peers. But 2024 looks set to be tougher. Further disinflation should support household spending power but tighter monetary policy is likely to bear down on households. Despite a smaller proportion of outstanding mortgages, the impact of the sharp rise in mortgage rates will be marked. It is also lagged, with more fixed deals than in previous cycles (Exhibit 1). This delayed the impact this year, but looks set to grow next, including via pass-throughs to rents (already rising at a double-digit pace) as buy-to-let landlords pass on higher borrowing costs.

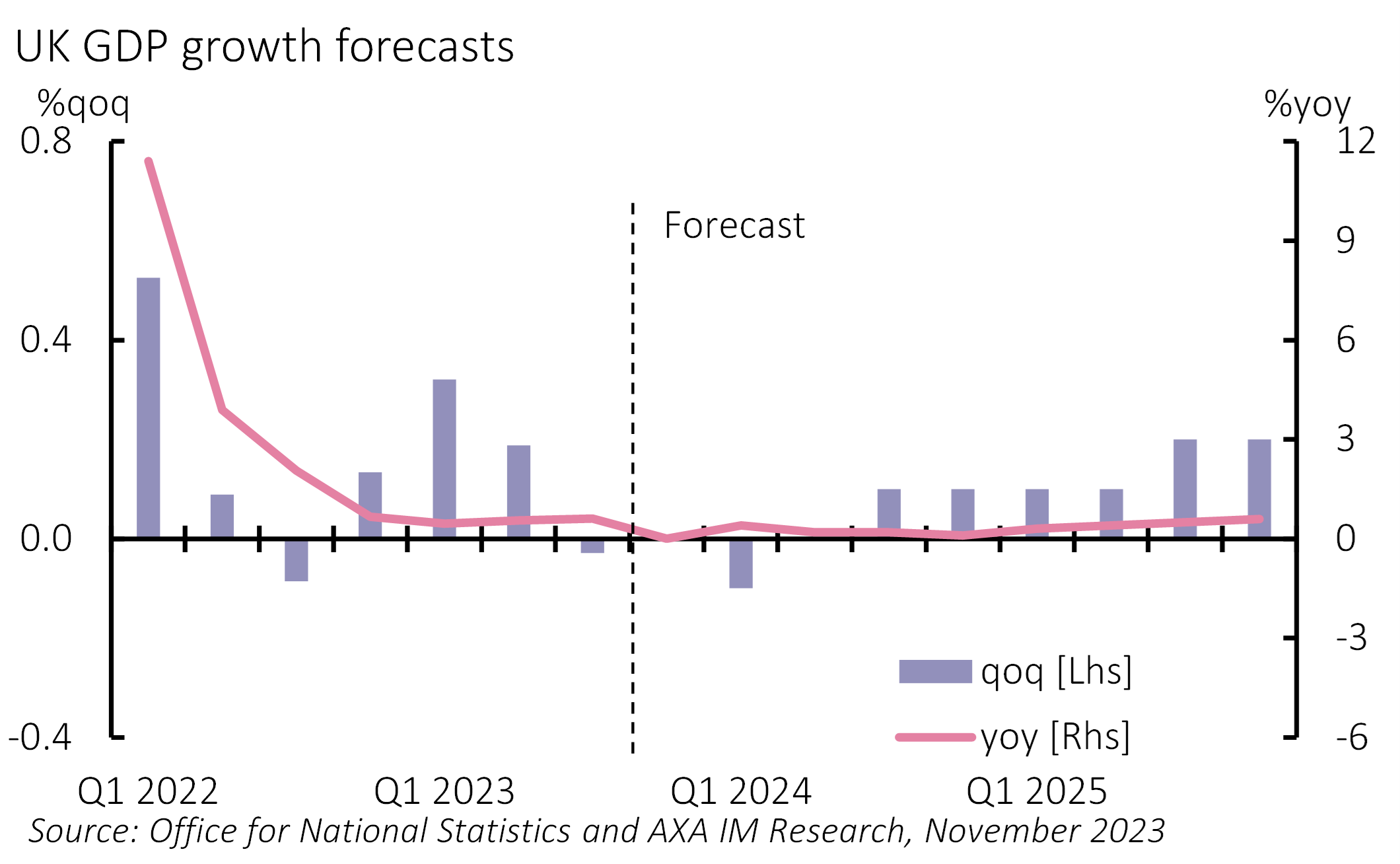

Exhibit 1: UK projected to narrowly avoid recession (again)

Weak consumer spending is likely to dominate the GDP outlook for 2024 and 2025. However, a weak cyclical outlook, elevated borrowing rates and political uncertainty, including infrastructure project cancellations and government commitment to climate change are also likely to contribute to weaker investment. We forecast GDP growth of 0.0% in 2024 and 0.5% in 2025 (from a forecast 0.5% in 2023). Our central view is perilously close to recession, with risks skewed in this direction. However, we forecast a modest acceleration in activity across 2025 as the pass-through of previous tightening ebbs and we anticipate fresh easing.

Weaker growth should loosen the labour market further. We forecast a rise in unemployment to 5% from 4.2% at present, a rise we see occurring sooner than the Bank of England (BoE) does. As such, we forecast wage growth slowing from an elevated 7.9% at present to below 4% by end-2025. Such an easing in labour conditions would help disinflation. The decline in inflation to date is because of a combination of falling energy inflation, slower food price inflation and a sharper fall in non-energy core goods. Services inflation remains elevated for now but has started to ease. The expected loosening in the labour market should see further services disinflation. We forecast inflation averaging 7.5% in 2023, 3.1% in 2024 and 1.8% in 2025. Our forecast sees inflation falling below target by mid-2025. We also recognise a risk that wage inflation remains stickier, which could delay broader services disinflation.

The BoE has left its benchmark interest rate at 5.25% since September and we think it has peaked. The lagged transmission of previous tightening is likely to tighten conditions further across 2024 and into 2025, even as spare capacity rises, and inflation falls. We expect the BoE to start easing policy in 2024 as its focus shifts to inflation falling below target the following year and being on track to remain there over its forecast horizon. We expect the BoE to confirm wage growth deceleration next spring before lowering interest rates by 25bp in August (with risks skewed to an earlier cut). We then forecast rate cuts to 4.50% by end-2024 and to 3.75% by mid-2025 – a sharper reduction than markets currently expect. We also expect the BoE to maintain quantitative tightening through 2025, with a broadly stable pace of active sales.

The UK is also due a General Election within the coming two years – most likely in October 2024. Polls and recent by-elections point to a Labour government for now, although the current Conservative government has a sizeable majority. Both parties are once again competing over the centre ground (having diverged to extremes over the last decade). A centrist government and significant fiscal constraints should limit the differences either new government has on the economy for 2025. We expect a modest fiscal easing (around 0.5% of GDP) in March. A new government is likely to need to tighten significantly in the first few years of the next term, which may add to a loosening monetary policy dynamic.

Avertissement de risque

La valeur des investissements, et les revenus qu'ils génèrent, peuvent aussi bien baisser qu'augmenter et les investisseurs peuvent ne pas récupérer le montant initialement investi.